Industrial Production in Manufacturing Update – 18 Month Outlook

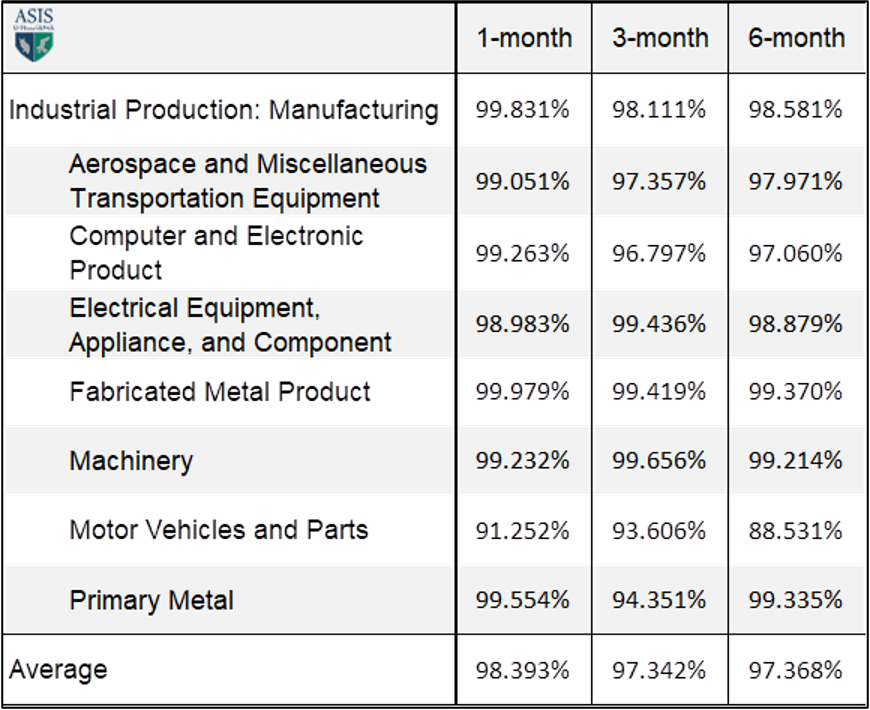

Posted By : Armada Corporate Intelligence | Date : January 12, 2024The Watch is a report that includes a set of predictive models covering more than 70% of US GDP. The capstone model is one that covers broad-based manufacturing overall, including both durable and nondurable manufacturing. Thus far, this model has performed well, coming in with 98.1% accuracy 3 months in advance and 98.6% accurate 6 months out. The following chart shows the performance of the primary sector models included in The Watch.

In addition, there are new models included in the outlook spanning retail sales and consumer spending (97.9% accuracy 6 months in advance), nonresidential construction (94.0% accuracy 6 months in advance), and the primary modes of transportation (to help companies understand forecasted transportation costs for the next 18 months). The trucking model is batting 93.7% 6 months out and rail carload is our highest performing model at 99.8% 6 months in advance.

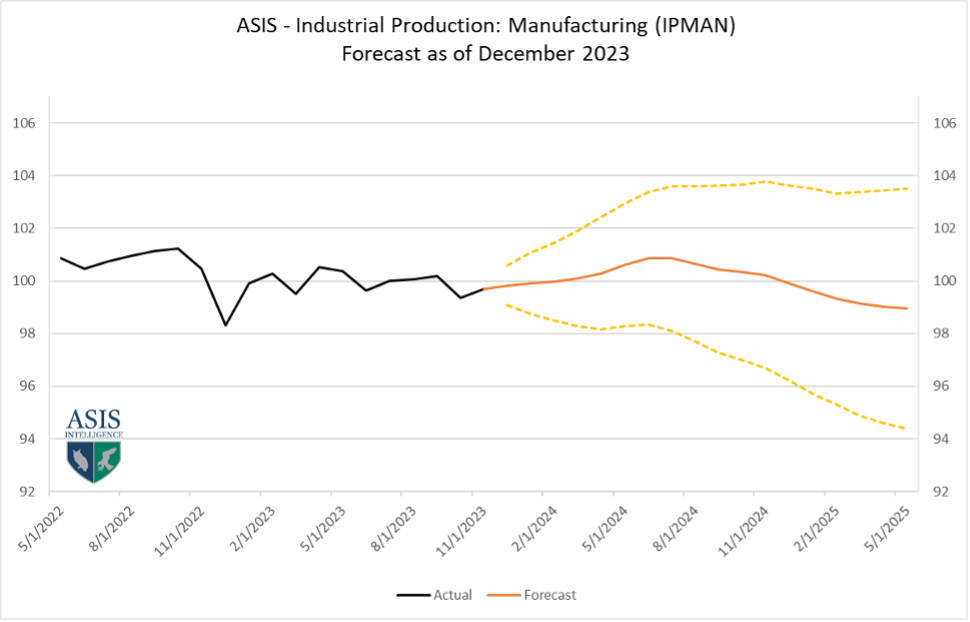

The latest model output for broad manufacturing shows what many of us have feared in manufacturing, there is a swoon of sorts in the model. The model predicts that the volume of manufacturing activity (on a broad basis) is likely to rise over the next three quarters through the middle of 2024 before beginning to drift off slightly late in 2024 and early in 2025.

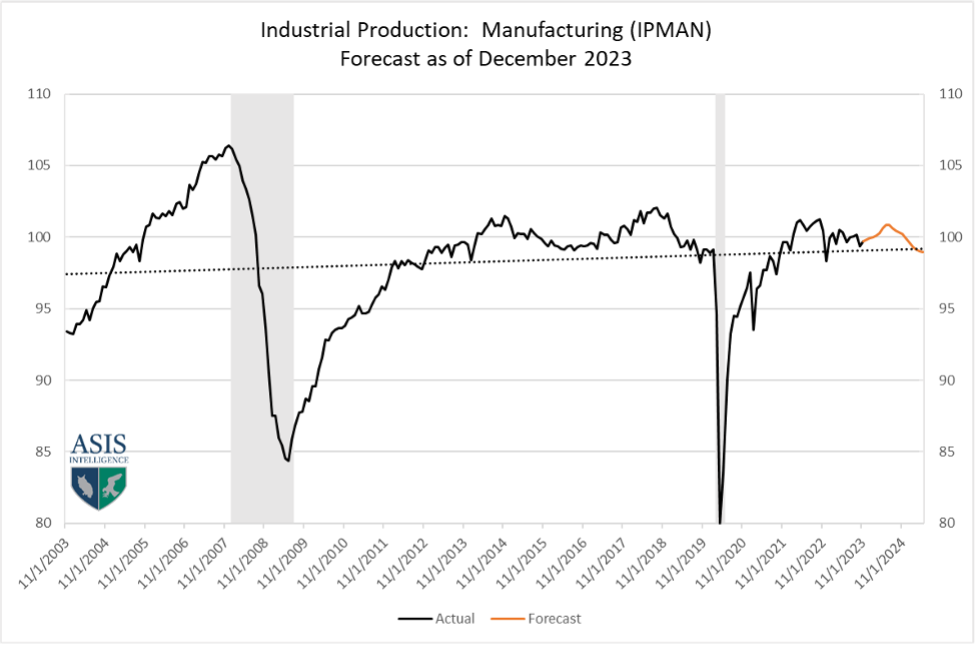

The long-term graph of the model shows the downturn a bit more dramatically. Although it can look a bit frightening at first blush, compared to other fluctuations over time, it is a mild downturn. We have seen similar downturns in periods between 2018 and late 2019 just prior to the pandemic. Most of us tend to look at the long term trendline (the black dotted line) and versus what we have seen historically, this would be considered to be a “mild softening” prediction for the sector, not recessionary on a historical basis. This would be akin to what many economists are predicting as a “soft landing” or “shallow recession” for the industrial production complex.

The global supply chain is shifting from a destocking period over the past 12 months into a more focused demand planning approach. Global supply chain congestion being spawned from the Red Sea, continued pressures in the Black Sea, Strait of Hormuz, and Panama Canal are all creating mild disruptions in activity. With this in mind, but with a global slowdown in manufacturing as a backdrop, companies are still going into the new year conservatively. New orders for products are sluggish and with interest rates sitting high on a historical basis, the cost of capital is high enough that companies are forced to keep inventories lean.

One of the important factors to understand is that these models are updated monthly. Each includes thousands of simulations that use up to 22 different economic metric inputs (modeled over 20 years) to develop these views. Although the data in the first 12 months is usually stable, the volatility shows up at the tail end of the curve between 13 and 18 months out.

Armada has other models also included in The Watch covering predictions for automotive, aerospace, computers and electronics, machinery, electrical equipment and appliances, fabricated metals, and primary metals. Interested parties can sign up for a free trial to The Watch (no credit card required) and the cost of subscription is inexpensive on a monthly basis (just $45 a month); and you can cancel at any time.