Long and Short of Consumer Price Index and Tariffs

Posted By : Armada Corporate Intelligence | Date : August 17, 2025The short answer on tariffs and inflation through the Consumer Price Index (CPI) is that they were having little impact. The bottom line is that tariff inflation was marginal at best and you really have to dig to find it.

If I had a discussion with most of you, you can all tell me where price inflation has hit you (or where you have passed it on to somebody). But at a macro level, it is being partially eaten throughout the supply chain and most of the impact is still muted.

I heard one of the staunchest opponents to tariffs say on Wednesday that they anticipate a one-time hit to inflation of 3 tenths of a percent pushing overall inflation (measured in the Fed’s favorite Personal Consumption Expenditures PCE – not in the CPI reflected in this article) to 3.1%. That’s nothing close to what we experienced in 2021-2023 during the global supply chain crisis. And even the Fed is forecasting it to quickly fall back down to 2.4% in 2026.

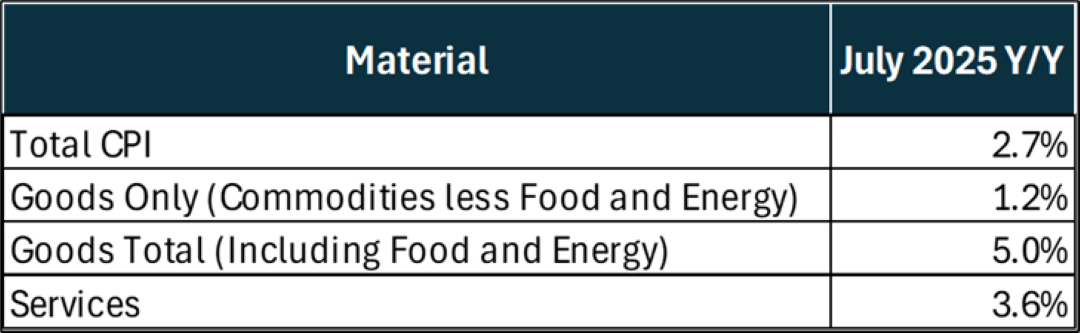

The latest data from the CPI showed headline inflation at just 2.7% annually. Looking for hints of tariff-induced inflation, it just wasn’t there. Goods only CPI when stripping out food and energy was growing at just 1.2%.

When we get aggressive with the figure, it jumps to 5%, but on the back of sharp increases in:

- Meat (primarily beef shortages)

- Coffee

- Sugar

- Food away from home (wage pressure)

- Natural gas (up 13.8%)

- Electricity (up 5.5%)

- Gasoline and oil were down (offsetting)

None of those were impacted by tariffs – all were impacted mostly by supply side issues.

Look, we can’t stop monitoring tariff inflation risk, but our attention is now shifting to other factors until/unless it starts to show up in the data. Based on what we hear from supply chain managers, there are still some price increases on the way. Here is how the market seems to be absorbing tariff rates:

- Suppliers eating part of it (~10%)

- Some of it absorbed in supply chain (carriers) (~10%)

- ~10% being eaten in margin

- Rest likely to be passed on

This current mix is likely not sustainable long term, eventually it will evolve into a one-time price adjustment (by Q4 or Q1 ‘26) because the suppliers and supply chain can’t continue to take deep discounts to soften the impact. But again, everyone agrees that it is a one-time, market price adjustment, and then future inflation risk will fall back on normal annual increases based on other market-based factors primarily tied to supply/demand.

That doesn’t change the fact that a T-shirt from a big box retailer might go from ~$4 to ~$5 in that one-time price hit, but the price will stick there, and the annual rate of change will fall back into a reasonable rate from then on. We just have to get through the initial adjustment – and the timing of it. And for now, perhaps those price increases are spread out over thousands of products, and they’ll hit at different times, but it isn’t having a material impact on the macro data at this point.

In either event, the Fed needs to move on and focus on other factors that are scarier – and get to rate trimming in my opinion. – KP