Conference Board’s LEI Flattens in July, Remains Low

Posted By : Armada Corporate Intelligence | Date : August 25, 2025The Conference Board’s Leading Economic Index report for July came in 0.1% lower month-over-month at 98.7. It was 2.7% lower over the last six months (which was faster than the 1% contraction seen in 2024). Keep in mind, the index had been showing the economy already under signs of stress in 2024, and trade uncertainty continued that stress in 2025 thus far.

Just for review, the LEI gives us a good indicator for which direction economic activity will be going in over the next 6 months. As the name implies, it is a look at the leading economic readings and the direction in which economy is headed.

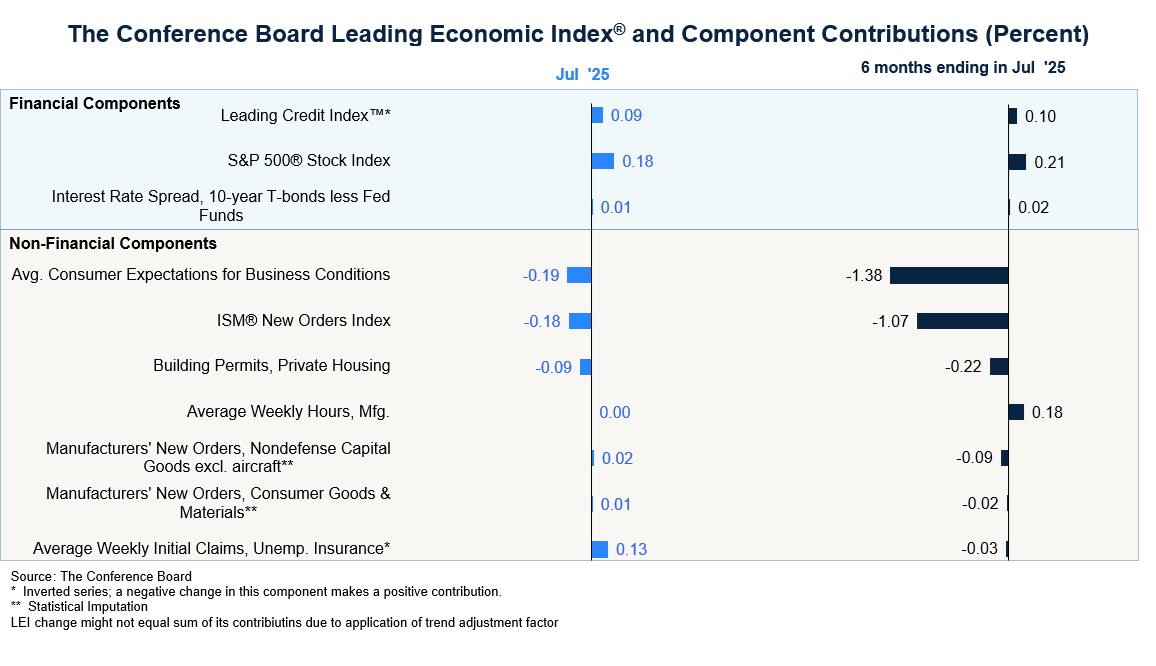

The chart below from the Conference Board shows both where the economy is accelerating and where it is facing headwinds. The greatest headwinds are coming from consumer sentiment, new orders indexes from the PMIs, and building permit softness.

Helping offset that to a degree is growth in the stock market (which typically carries some underpinnings of decent corporate profits with it) and some decent growth in average manufacturing hours.

The good news is that there were some signs of life in the S&P Global Flash PMI report for the US in new orders. Next week, we will get the official reports from both S&P Global and the ISM and should have a better understanding of whether there was some good momentum building in August, or if it was just an anomaly.

On the housing permit front, those are likely to remain lower until the Federal Reserve does something with interest rates, and a quarter-point cut is symbolic but won’t really move the needle. It may take 50-75 basis points in cuts to get some momentum in the housing market started, and the real impact won’t come until after 10-Year bond rates adjust. The Fed’s move to trim interest rates will eventually help the bond market, but there can often be a lag between interest rate cuts and easing bond yields. In addition, in 2024, we saw treasuries move in an opposite direction to the Fed’s lowering of the Effective Fed Funds Rate. Remember that long-term treasuries hate inflation and deficits (oversimplifying). Both of which are still showing signs of risk. – KP